The Russian economy is near stagnation, with continued depressed

domestic demand leading to growth of 0.8 % in the first half of 2014, similar

to 0.9% in 2013. It was operating on the threshold of recession in the first

half of 2014 with quarterly seasonally adjusted growth for the first two

quarters close to zero. As a result, Russia’s growth dipped in the first

quarter under that of all other relevant comparator country groups. Consumer

and business sentiments were already weak in 2013 due to lingering structural

problems and contributed to the wait-and-see attitudes of households and companies

and leading to a slowdown of the Russian economy to 1.3% from 3.4 %in 2012.

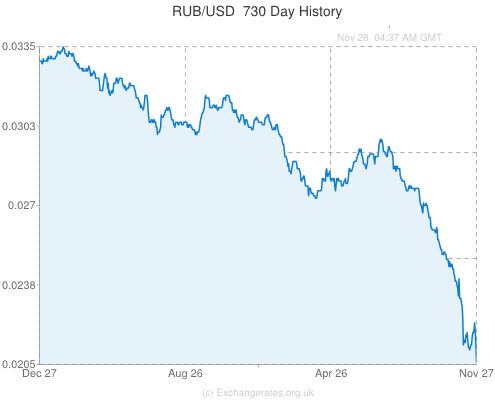

I past three month Russian currency ruble has fallen upto

23% against USD. Such a plunge inevitably brings inflation in the form of more

expensive imports, a worry given that consumer prices in Russia are already

rising at over 8% a year.

I past three month Russian currency ruble has fallen upto

23% against USD. Such a plunge inevitably brings inflation in the form of more

expensive imports, a worry given that consumer prices in Russia are already

rising at over 8% a year.

The head of the Central Bank of Russia, Elvira Nabiullina,

is struggling to nip this trend in the bud. First, on November 5th, she hiked

interest rates, to 9.5%. That means that rouble deposits earn far more than

dollar ones, which should make the currency more attractive. Next, she

attempted to deter bets against the rouble by replacing the central bank’s puny

and predictable sale of $350m a day in its defence with the threat of far bigger

ad hoc interventions. Finally, she crimped commercial banks’ access to roubles

to limit their ability to speculate against the currency.

While making changes Ms Nabiullina needed to be more courageous.

The main reseaon ofr The first is oil.

In the first half of 2014 Russia’s exports brought in $255 billion, with 68% of

that coming from sales of oil and natural gas. During that period oil prices

averaged $109 a barrel; today they are close to $80. Applying a proportional

cut to Russia’s energy exports would slash revenues by over $40 billion, more

than wiping out Russia’s current-account surplus.

There are other reasons to sell roubles and buy dollars.

Across the economy there is over $120 billion in external debt maturing in the

next year according to central bank data.

The dependence on Western markets and currencies pains

Vladimir Putin, Russia’s president. On November 10th he signed a deal with Xi

Jinping, his Chinese counterpart, that will see Russia export gas from Siberia

to China via new pipelines. The deal provides a huge new source of demand, and

could see China replace Europe as Russia’s main export market.

But the pipelines will take years to be built and financing

for the project has yet to be secured. In the meantime Russia may have to cope

with low oil and gas prices for years. On November 12th a new set of forecasts

from the Energy Information Administration, an American government agency, said

that oil prices are likely to average $83 a barrel in 2015.

If VLADIMIR PUTIN is not short of problems and many of them

are his own creation. There is the carnage in eastern Ukraine, where he is

continuing to stir things up. There are his fraught relations with the West,

with even Germany turning against him now. There is an Islamist insurgency on

his borders and at home there is grumbling among the growing numbers who doubt

the wisdom of his Ukraine policy.

Russia’s oil-fired economy surged upward on rising energy

prices; now that oil has tumbled, from an average of almost $110 a barrel in

the first half of the year to below $80, Russia is hurting. More than

two-thirds of exports come from energy.

The immediate worry is the oil price. Mr Putin is confident

it will make progress. But supply seems set to increase, with OPEC keen to

defend its market share. American government agencies predict oil prices could

average $83 a barrel in 2015, well below the $90 level Russia needs to avoid

recession (by keeping its budget in balance). If global demand weakens—Japan

has slipped into recession since the latest round of forecasts—the oil price

could fall further. That would immediately prompt investors to reassess

Russia’s prospects.

Russia’s firms have over $500 billion in external debt

outstanding, with $130 billion of it payable before the end of 2015, at a time

when few Western banks want to increase their exposure to Russia.

Russia’s public finances are also much healthier than those

of many of the countries against which it is pitted over Ukraine. The budget

deficit was 1.3% of GDP last year, whereas it stood at 3.3% for the EU.

Government debt amounted to a mere 13% of GDP, compared with 87% in the EU.

Russia’s current account is in surplus, forecast by the IMF

to be 2.1% of GDP in 2014. In contrast countries like Turkey and South Africa,

which took a battering earlier this year as investors worried about fragile

emerging economies, are projected to run deficits of 6.3% and 5.4%

respectively.

Russia’s economy is teetering on the verge of recession. The

central bank says it expects the next two years to bring no growth. Inflation

is on the rise. The rouble has lost 30% of its value since the start of the

year, and with it the faith of the country’s businessmen. Banks have been cut

off from Western capital markets, and the price of oil—Russia’s most important

export commodity—has fallen hard. Consumption, the main driver of growth in the

previous decade, is slumping. Money and people are leaving the country.

In 2007, when oil

was $72 a barrel, the economy managed to grow

Between 2010 and 2013, when oil prices were high, the country’s net outflow of capital was $232 billion—20 times what it was between 2004 and 2008. Russian economists are now debating how long before the economy faces collapse. Most think it can totter on for two years or so.

But there is a real chance things could get a lot worse a lot sooner. The depreciation of the rouble, which closely tracks the oil price, has helped Russia cushion its budget as that price has slumped (see chart). When the oil price falls, so does the rouble; thus in rouble terms the amount of money the oil brings in stays roughly the same. But it cannot buy as much. Russia imports a great deal—the total value of imported goods, $45 billion in 2000, was $341 billion in 2013—and so a devalued rouble quickly stokes inflation. It is predicted to reach 9% by the end of this year; for food the rate is higher still. If it is to compensate the population for this loss in its spending power, the government will have to run a bigger deficit. If it does not it will face discontent. A weak rouble also makes servicing foreign debt more expensive. Russia’s sovereign debt is just $57 billion, but its corporate debt is ten times as high. Some of it has been racked up by state corporations and national energy companies, which gives it a quasi-sovereign status. And by the end of 2015 Russian firms will have to repay about $130 billion of foreign debt.

A return to higher growth in Russia will depend on solid

private investment growth and a lift in consumer sentiment, which will require

creating a predictable policy environment and addressing the unresolved

structural reform agenda.

Current market condition

Please write me on my Email id:-

divyanalysis@gmail.com

Or subscribes me my facebook page:-

https://www.facebook.com/Divyanalysi

Current market condition

.png)

divyanalysis@gmail.com

Or subscribes me my facebook page:-

https://www.facebook.com/Divyanalysi

No comments:

Post a Comment